Financial Accounting Unit I eNotes BCOM SEM I

BCOM NEP SEM I

Financial Accounting

lucknow University

Free Notes

Unit I : Definition, Nature and Scope of Accounting, Concepts and Conventions, Introduction to Financial Statements, Capital and Revenue Items, Indian Accounting Standards & IFRS.

Meaning of Accounting

In 1941, The American Institute of Certified Public Accountants (AICPA) had defined accounting as the art of recording, classifying, and summarising in a significant manner and in terms of money, transactions and events which are, in part at least, of financial character, and interpreting the results thereof’. With greater economic development resulting in changing role of accounting, its scope, became broader. In 1966, the American Accounting Association (AAA) defined accounting as ‘the process of identifying, measuring and communicating economic information to permit informed judgments and decisions by users of information’. In 1970, the Accounting Principles Board of AICPA also emphasised that the function of accounting is to provide quantitative information, primarily financial in nature, about economic entities, that is intended to be useful in making economic decisions.

Accounting can therefore be defined as the process of identifying, measuring, recording and communicating the required information relating to the economic events of an organisation to the interested users of such information. In order to appreciate the exact nature of accounting, we must understand the following relevant aspects of the definition:

• Economic Events

• Identification, Measurement, Recording and Communication

• Organisation

• Interested Users of Information

Economic Events

Business organisations involve economic events. An economic event is known as a happening of consequence to a business organisation which consists of transactions and which are measurable in monetary terms. For example, purchase of machinery, installing and keeping it ready for manufacturing is an event which comprises number of financial transactions such as buying a machine, transportation of machine, site preparation for installation of a machine, expenditure incurred on its installation and trial runs. Thus, accounting identifies bunch of transactions relating to an economic event. If an event involves transactions between an outsider and an organisation, these are known as external events.Identification, Measurement, Recording and Communication Identification : It means determining what transactions to record, i.e., to identity events which are to be recorded. It involves observing activities and selecting those events that are of considered financial character and relate to the organisation. The business transactions and other economic events therefore are evaluated for deciding whether it has to be recorded in books of account. For example, the value of human resources, changes in managerial policies or appointment of personnel are important but none of these are recorded in books of account. However, when a company makes a sale or purchase, whether on cash or credit, or pays salary it is recorded in the books of account.

Organisation

Organisation refers to a business enterprise, whether for profit or not-forprofit motive. Depending upon the size of activities and level of business operation, it can be a sole proprietory concern, partnership firm, cooperative society, company, local authority, municipal corporation or any other association of persons.

Interested Users of Information

Accounting is a means by which necessary financial information about business enterprise is communicated and is also called the language of business. Many users need financial information in order to make important decisions. These users can be divided into two broad categories: internal users and external users. Internal users include: Chief Executive, Financial Officer, Vice President, Business Unit Managers, Plant Managers, Store Managers, Line Supervisors, etcBranches of Accounting

The economic development and technological advancements have resulted in an increase in the scale of operations and the advent of the company form of business organisation. This has made the management function more and more complex and increased the importance of accounting information. This gave rise to special branches of accounting. These are briefly explained below:

1. Financial accounting:

The purpose of this branch of accounting is to keep a record of all financial transactions so that:

• the profit earned or loss sustained by the business during an accounting period can be worked out,

• the financial position of the business as at the end of the accounting period can be ascertained, and

• the financial information required by the management and other interested parties can be provided.

2. Cost Accounting:

The purpose of cost accounting is to analyse the expenditure so as to ascertain the cost of various products manufactured by the firm and fix the prices. It also helps in controlling the costs and providing necessary costing information to management for decision-making.

3. Management Accounting:

The purpose of management accounting is to assist the management in taking rational

policy decisions and to evaluate the impact of its decisons and actions.

Generally Accepted Accounting Principles

In order to maintain uniformity and consistency in accounting records, certain rules or principles have

been developed which are generally accepted by the accounting profession.

These rules are called by different names such as principles, concepts, conventions, postulates,

assumptions and modifying principles.

The Generally Accepted Accounting Principles have evolved over a long period of time on the basis of

past experiences, usages or customs, statements by individuals and professional bodies and regulations

by government agencies and have general acceptability among most accounting professionals.

However, the principles of accounting are not static in nature.

These are constantly influenced by changes in the legal, social and economic environment as well as

the needs of the users.

Basic Accounting Concepts

The basic accounting concepts are referred to as the fundamental ideas or basic assumptions underlying the theory and practice of financial accounting and are broad working rules for all accounting activities and developed by the accounting profession. The important concepts have been listed as below:

1) Business entity;

2) Money measurement;

3) Going concern;

4) Accounting period;

5) Cost

6) Dual aspect (or Duality);

7) Revenue recognition (Realisation);

8) Matching;

9) Full disclosure;

10) Consistency;

11) Conservatism (Prudence);

12) Materiality;

13) Objectivity.

1. Business Entity Concept

The concept of business entity assumes that business has a distinct and separate entity from its owners. It means that for the purposes of accounting, the business and its owners are to be treated as two separate entities. Keeping this in view, when a person brings in some money as capital into his business, in accounting records, it is treated as liability of the business to the owner. Here, one separate entity (owner) is assumed to be giving money to another distinct entity (business unit). Similarly, when the owner withdraws any money from the business for his personal expenses(drawings), it is treated as reduction of the owner’s capital and consequently a reduction in the liabilities of the business. The accounting records are made in

2. Money Measurement Concept

The concept of money measurement states that only those transactions and happenings in an organisation which can be expressed in terms of money such as sale of goods or payment of expenses or receipt of income, etc. are to be recorded in the book of accounts. All such transactions or happenings which can not be expressed in monetary terms, for example, the appointment of a manager, capabilities of its human resources or creativity of its research department or image of the organisation among people in general do not find a place in the accounting records of a firm.

3. Going Concern Concept

The concept of going concern assumes that a business firm would continue to carry out its operations indefinitely, i.e. for a fairly long period of time and would not be liquidated in the foreseeable future. This is an important assumption of accounting as it provides the very basis for showing the value of assets in the balance sheet.

4. Accounting Period Concept

Accounting period refers to the span of time at the end of which the financial statements of an enterprise are prepared, to know whether it has earned profits or incurred losses during that period and what exactly is the position of its assets and liabilities at the end of that period. Such information is required by different users at regular interval for various purposes, as no firm can wait for long to know its financial results as various decisions are to be taken at regular intervals on the basis of such information. The financial statements are, therefore, prepared at regular interval, normally after a period of one year, so that timely information is made available to the users. This interval of time is called accounting period.

5. Cost Concept

The cost concept requires that all assets are recorded in the book of accounts at their purchase price, which includes cost of acquisition, transportation installation and making the asset ready to use. To illustrate, on June 2005, an old plant was purchased for Rs. 50 lakh by Shiva Enterprise, which is into the business of manufacturing detergent powder. An amount of Rs. 10,000 was spent on transporting the plant to the factory site. In addition, Rs. 15,000 was spent on repairs for bringing the plant into running position and Rs. 25,000 on its installation. The total amount at which the plant will be recorded in the books of account would be the sum of all these, i.e. Rs. 50,50,000.

6. Dual Aspect Concept

Dual aspect is the foundation or basic principle of accounting. It provides the very basis for recording business transactions into the book of accounts. This concept states that every

transaction has a dual or two-fold effect and should therefore be recorded at two places. In other words, at least two accounts will be involved in recording a transaction. This can be explained with the help of an example. Ram started business by investing in a sum of Rs. 50,00,000 The amount of money brought in by Ram will result in an increase in the assets (cash) of business by Rs. 50,00,000. At the same time, the owner’s equity or capital will also increase by an equal amount. It may be seen that the two items that got affected by this transaction are cash and capital account.

7. Revenue Recognition (Realisation) Concept

The concept of revenue recognition requires that the revenue for a business transaction should be included in the accounting records only when it is realised. Here arises two questions in mind. First, is termed as revenue and the other, when the revenue is realised. Let us take the first one first. Revenue is the gross inflow of cash arising from (i) the sale of goods and services by an enterprise; and (ii) use by others of the enterprise’s resources yielding interest, royalties and dividends. Secondly, revenue is assumed to be realised when a legal right to receive it arises, i.e. the point of time when goods have been sold or service has been rendered.

8. Matching Concept

The process of ascertaining the amount of profit earned or the loss incurred during a particular period involves deduction of related expenses from the revenue earned during that period. The matching concept emphasises exactly on this aspect. It states that expenses incurred in an accounting period should be matched with revenues during that period. It follows from this that the revenue and expenses incurred to earn these revenues must belong to the same accounting period.

9. Full Disclosure Concept

Information provided by financial statements are used by different groups of people such as investors, lenders, suppliers and others in taking various financial decisions. In the corporate form of organisation, there is a distinction between those managing the affairs of the enterprise and those owning it. Financial statements, however, are the only or basic means of communicating financial information to all interested parties. It becomes all the more important, therefore, that the financial statements makes a full, fair and adequate disclosure of all information which is relevant for taking financial decisions.

10. Consistency Concept

The accounting information provided by the financial statements would be useful in drawing conclusions regarding the working of an enterprise only when it allows comparisons over a period of time as well as with the working of other enterprises. Thus, both inter-firm and inter period comparisons are required to be made. This can be possible only when accounting policies and practices followed by enterprises are uniform and are consistent over the period of time.

11. Conservatism Concept

The concept of conservatism (also called ‘prudence’) provides guidance for recording transactions in

12. Materiality Concept

The concept of materiality requires that accounting should focus on material facts. Efforts should not be wasted in recording and presenting facts, which are immaterial in the determination of income. The question that arises here is what is a material fact. The materiality of a fact depends on its nature and the amount involved. Any fact would be considered as material if it is reasonably believed that its knowledge would influence the decision of informed user of financial statements. For example, money spent on creation of additional capacity of a theatre would be a material fact as it is going to increase the future earning capacity of the enterprise. Similarly, information about any change in the method of depreciation adopted or any liability which is likely to arise in the near future would be significant information.

13. Objectivity Concept

The concept of objectivity requires that accounting transaction should be recorded in an objective manner, free from the bias of accountants and others. This can be possible when each of the transaction is supported by verifiable documents or vouchers. For example, the transaction for the purchase of materials may be supported by the cash receipt for the money paid, if the same is purchased on cash or copy of invoice and delivery challan, if the same is purchased on credit. Similarly, receipt for the amount paid for purchase of a machine becomes the documentary evidence for the cost of machine and provides an objective basis for verifying this transaction. One of the reasons for the adoption of ‘Historical Cost’ as the basis of recording accounting transaction is that adherence to the principle of objectivity is made possible by it. As stated above, the cost actually paid for an asset can be verified from the documents but it is very difficult to ascertain the market value of an asset until it is actually sold. Not only that, the market value may vary from person to person and from place to place, and so ‘objectivity’ cannot be maintained if such value is adopted for accounting purposes.

Financial Statements

Financial statements are written records that convey the business activities and the financial performance

of a company. Financial statements are often audited by government agencies, accountants, firms, etc.

to ensure accuracy and for tax, financing, or investing purposes.

It has been emphasised that various users have diverse informational requirements.

Instead of generating particular information useful for specific users, the business prepares a set of

financial statements, which in general satisfies the informational needs of the users.

The basic objectives of preparing financial statements are:

(a) To present a true and fair view of the financial performance of the business;

(b) To present a true and fair view of the financial position of the business; and For this purpose, the firm usually prepares the following financial statements:

1. Trading and Profit and Loss Account

2. Balance Sheet

3. Cash flow statement.

Key features of Financial Statements

• Financial statements are written records that convey the business activities and the financial performance of a company.

• The balance sheet provides an overview of assets, liabilities, and stockholders' equity as a snapshot in time.

• The income statement primarily focuses on a company’s revenues and expenses during a particular period. Once expenses are subtracted from revenues, the statement produces a company's profit figure called net income.

• The cash flow statement (CFS) measures how well a company generates cash to pay its debt obligations, fund its operating expenses, and fund investments.

Here we will discuss only

1. Trading and Profit and Loss Account

2. Balance Sheet.

Trading and Profit and Loss account, also known as Income statement, shows the financial performance in the form of profit earned or loss sustained by the business. Balance Sheet shows financial position in the form of assets, liabilities and capital. These are prepared on the basis of trial balance and additional information, if any.

Trading and Profit and Loss Account

Trading and Profit and Loss account is prepared to determine the profit earned or loss sustained by the business enterprise during the accounting period. It is basically a summary of revenues and expenses of the business and calculates the net figure termed as profit or loss. Profit is revenue less expenses. If expenses are more than revenues, the figure is termed as loss. Trading and Profit and Loss account summarises the performance for an accounting period. It is achieved by transferring the balances of revenues and expenses to the trading and profit and loss account from the trial balance. Trading and Profit and Loss account is also an account with Debit and Credit sides. It can be observed that debit balances (representing expenses) and losses are transferred to the debit side of the Trading and a Profit and Loss account and creditnbalance (representing revenues/gains) are transfered to its credit side.

Relevant Items in Trading and Profit and Loss Account

The different items appearing in the trading and profit and loss account are explained hereunder:

Items on the debit side

(i) Opening stock: It is the stock of goods in hand at the beginning of the accounting year. This is the stock of goods which has been carried forward from the previous year and remains unchanged during the year and appears in the trial balance. In the trading account it appears on the debit side because it forms the part of cost of goods sold for the current accounting year.

(ii) Purchases less returns: Goods, which have been bought for resale appears as purchases on the debit side of the trading account. They include both cash as well as credit purchases. Goods which are returned to suppliers are termed as purchases return. It is shown by way of deduction from purchases and the computed amount is known as Net purchases.

(iii) Wages: Wages refer to remuneration paid to workers who are directly engaged in factory for loading, unloading and production of goods and are debited to trading account.

(iv) Carriage inwards/Freight inwards: These expenses are the items of transport expenses, which are incurred on bringing materials/goods purchased to the place of business. These items are paid in respect of purchases made during the year and are debited to the trading account.

(v) Fuel/Water/Power/Gas: These items are used in the production process and hence are part of expenses.

(vi) Packaging material and Packing charges: Cost of packaging material used in the product are direct expenses as it refers to small containers which form part of goods sold. However, the packing refers to the big containers that are used for transporting the goods and is regarded as an indirect expense debited to profit and loss account.

(vii) Salaries: These include salaries paid to the administration, godown and warehouse staff for the services rendered by them for running the business. If salaries are paid in kind by providing certain facilities (called perks) to the employees such as rent free accommodation, meals, uniform, medical facilities should also be regarded as salaries and debited to the profit and loss account.

(viii) Rent paid: These include office and godown rent, municipal rates and taxes, factory rent, rates and taxes. The amount of rent paid is shown on the debit side of the profit and loss account.

(ix) Interest paid: Interest paid on loans, bank overdraft, renewal of bills of exchange, etc. is an expense and is debited to profit and loss account.

(x) Commission paid: Commission paid or payable on business transactions undertaken through the agents is an item of expense and is debited to profit and loss account.

(xi) Repairs: Repairs and small renewals/ replacements relating to plant and machinery, furniture, fixtures, fittings, etc. for keeping them in working condition are included under this head. Such expenditure is debited to profit and loss account.

(xii) Miscellaneous expenses: Though expenses are classified and booked under different heads, but certain expenses being of small amount clubbed together and are called miscellaneous expenses. In normal usage these expenses are called Sundry expenses or Trade expenses.

Items on the credit side

(i) Sales less returns: Sales account in trial balance shows gross total sales(cash as well as credit) made during the year. It is shown on the credit side of the trading account. Goods returned by customers are called return inwards and are shown as deduction from total sales and the computed amount is known as net sales.

(ii) Other incomes: Besides salaries and other gains and incomes are alsorecorded in the profit and loss account. Examples of such incomes are rent received, dividend received, interest received, discount received, commission received, etc

Concept of Gross Profit and Net Profit

The trading and profit and loss can be seen as combination of two accounts, viz. Trading account and Profit and Loss account. The trading account or the first part ascertains the gross profit and profit and loss account or the second part ascertains net profit.

Profit and Loss (P&L) Statement

A P&L statement, often referred to as the income statement, is a financial statement that summarizes the revenues, costs, and expenses incurred during a specific period of time, usuallya fiscal year or quarter. These records provide information about a company's ability (or lack thereof) to generate profit by increasing revenue, reducing costs, or both. The P&L statement's many monikers include the "statement of profit and loss," the "statement of operations," the "statement of financial results," and the "income and expense statement." The profit and loss (P&L) statement is a financial statement that summarizes the revenues, costs, and expenses incurred during a specified period, usually a fiscal quarter or year. The P&L statement is synonymous with the income statement. These records provide information about a company's ability or inability to generate profit by increasing revenue, reducing costs, or both. Some refer to the P&L statement as a statement of profit and loss, income statement, statement of operations, statement of financial results or income, earnings statement or expense statement. P&L management refers to how a company handles its P&L statement through revenue and cost management.

The P&L statement is one of three financial statements every public company issues quarterly and annually, along with the balance sheet and the cash flow statement. It is often the most popular and common financial statement in a business plan as it quickly shows how much profit or loss was generated by a business. The income statement, like the cash flow statement, shows changes in accounts over a set period. The balance sheet, on the other hand, is a snapshot, showing what the company owns and owes at a single moment. It is important to compare the income statement with the cash flow statement since, under the accrual method of accounting, a company can log revenues and expenses before cash changes hands. The income statement follows a general form as seen in the example below. It begins with an entry for revenue, known as the top line, and subtracts the costs of doing business, including the cost of goods sold, operating expenses, tax expenses, and interest expenses. The difference, known as the bottom line, is net income, also referred to as profit or earnings. You can find many templates for creating a personal or business P&L statement online for free. It is important to compare income statements from different accounting periods, as the changes in revenues, operating costs, research and development spending, and net earnings over time are more meaningful than the numbers themselves. For example, a company's revenues may grow, but its expenses might grow at a faster rate.

Key Features of Profit and Loss Account

The P&L statement is a financial statement that summarizes the revenues, costs, and expenses incurred during a specified period.

∙ The P&L statement is one of three financial statements every public company issues quarterly and annually, along with the balance sheet and the cash flow statement. ∙ It is important to compare P&L statements from different accounting periods, as the changes in revenues, operating costs, R&D spending, and net earnings over time are more meaningful than the numbers themselves.

∙ Together with the balance sheet and cash flow statement, the P&L statement provides an in-depth look at a company's financial performance.

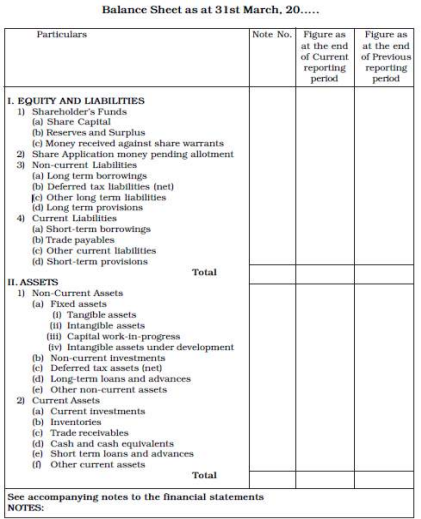

Balance Sheet

A balance sheet is a financial statement that reports a company's assets, liabilities and shareholders' equity at a specific point in time, and provides a basis for computing rates of return and evaluating its capital structure. It is a financial statement that provides a snapshot of what a company owns and owes, as well as the amount invested by shareholders. The balance sheet is used alongside other important financial statements such as the income statement and statement of cash flows in conducting fundamental analysis or calculating financial ratios. The balance sheet is a snapshot representing the state of a company's finances at a moment in time. By itself, it cannot give a sense of the trends that are playing out over a longer period. For this reason, the balance sheet should be compared with those of previous periods. It should also be compared with those of other businesses in the same industry since different industries have unique approaches to financing. A number of ratios can be derived from the balance sheet, helping investors get a sense of how healthy a company is. These include the debt-to-equity ratio and the acid-test ratio, along with many others. The income statement and statement of cash flows also provide valuable context for assessing a company's finances, as do any notes or addenda in an earnings report that might refer back to the balance sheet. Balance Sheet is one of the reports of a financial statement which provides the financial condition on a given date. An entity’s balance sheet provides a lot of information which can be used to analyse the financial stability and business performance. The balance sheet is a report version of the accounting equation that is balance sheet equation where the total of assets always is equal to the total of liabilities plus shareholder’s capital.

Assets = Liability + Capital

Investors and creditors generally look at the balance sheet and infer as to how efficiently an entity can use its resources and assess the value of their investments.

The three important sections of any balance sheet are:

• Assets – This is a resource owned by an entity to produce positive economic value.

• Liabilities – This provides a list of debts an entity owes to others.

• Capital or Equity- This is the amount invested by the shareholders

Importance of Balance Sheet

Balance sheet analysis can reveal a lot of important information about a company’s

Key Features of Profit and Loss Account

∙ The P&L statement is a financial statement that summarizes the revenues, costs, and expenses incurred during a specified period.

∙ The P&L statement is one of three financial statements every public company issues quarterly and annually, along with the balance sheet and the cash flow statement. ∙ It is important to compare P&L statements from different accounting periods, as the changes in revenues, operating costs, R&D spending, and net earnings over time are more meaningful than the numbers themselves.

∙ Together with the balance sheet and cash flow statement, the P&L statement provides an in-depth look at a company's financial performance.

Balance Sheet

A balance sheet is a financial statement that reports a company's assets, liabilities and shareholders' equity at a specific point in time, and provides a basis for computing rates of return and evaluating its capital structure. It is a financial statement that provides a snapshot of what a company owns and owes, as well as the amount invested by shareholders. The balance sheet is used alongside other important financial statements such as the income statement and statement of cash flows in conducting fundamental analysis or calculating financial ratios. The balance sheet is a snapshot representing the state of a company's finances at a moment in time. By itself, it cannot give a sense of the trends that are playing out over a longer period. For this reason, the balance sheet should be compared with those of previous periods. It should also be compared with those of other businesses in the same industry since different industries have unique approaches to financing. A number of ratios can be derived from the balance sheet, helping investors get a sense of how healthy a company is. These include the debt-to-equity ratio and the acid-test ratio, along with many others. The income statement and statement of cash flows also provide valuable context for assessing a company's finances, as do any notes or addenda in an earnings report that might refer back to the balance sheet. Balance Sheet is one of the reports of a financial statement which provides the financial condition on a given date. An entity’s balance sheet provides a lot of information which can be used to analyse the financial stability and business performance. The balance sheet is a report version of the accounting equation that is balance sheet equation where the total of assets always is equal to the total of liabilities plus shareholder’s capital.

Assets = Liability + Capital

Investors and creditors generally look at the balance sheet and infer as to how efficiently an entity can use its resources and assess the value of their investments.

The three important sections of any balance sheet are:

• Assets – This is a resource owned by an entity to produce positive economic value.

• Liabilities – This provides a list of debts an entity owes to others.

• Capital or Equity- This is the amount invested by the shareholders

Importance of Balance Sheet

Balance sheet analysis can reveal a lot of important information about a company’s performance. Importance of balance sheet is listed below:

• It is an important tool used by outsiders such as investors, creditors, and other stakeholders to understand the financial health of an entity.

• It is a tool to measure the growth of an entity. This can be done by comparing the balance sheet of different years.

• It is an essential document that must be submitted to the bank or investors to obtain a business loan.

• It helps stakeholders to understand the business performance and liquidity position of the entity.

Capital and Revenue Items

In order to know the fair performance and financial standing of a business; the nature of business transactions taking place during the year has to be analysed. The accounting transactions may be divided into two categories:

(1) Capital transactions (relating to capital items)

(2) Revenue transactions (relating to revenue items)

Definition of Capital Items:

Capital items are those items which have long term effects on business, (normally more than one year). There are two main types of of capital items; (i) capital expenditure and (ii) capital receipt. For example, fixed assets; tangible or intangible assets; (land, building, machinery, legal rights, etc) are capital items.

Definition Revenue Items:

Revenue items are those items having short term effects on business, (normally less than one year). There are two main types of revenue items; (i) revenue expenditure and (ii) revenue receipts. For example, repairs, wages, salaries, fuel, etc., are revenue items.

Treatment of Capital and Revenue Items in Financial Statements:

• Capital expenditure = Shown as a non-current asset in the balance sheet.

• Revenue expenditure = Shown as an expense in the income statement.

• Capital receipt = Shown as a liability or reduce the value of a capital expenditure.

• Revenue receipt = Shown as income in income statement

Indian Accounting Standards

Ind AS stands for Indian Accounting Standard and is converged standards for IFRS (International Financial Reporting Standards). Ind AS are documents and policies that provide principles for recognition, measurement, treatment, presentation and disclosures of accounting transactions in the Ind AS financial statements. For example: Ind AS 16 on Property, Plant and Equipment (PPE) will provide principles on the criteria on the basis of which PPE is recognised, what all cost will form part of PPE, how to treat those cost and how to present PPE in the financial statement and relevant disclosures. Ind AS are prepared keeping IFRS in mind, in actual these are IFRS in their converged form.There are 41 Ind AS notified till now.

Objective of Indian Accounting Standards:

Before the introduction of Ind AS, financial statements were prepared on the basis of Accounting Standards (AS) which were not in line with the standards and principles applicable globally (IFRS). Due to this investors were not able to assess and compare the financial position of Indian companies with other global companies. In order to make the financial statements uniform, Ind AS were introduced which are converged form of IFRS (global standards). Moreover, introduction of Ind AS will bring consistency in the accounting practices and principles followed by companies in India and other companies across world, leading to enhanced accessibility and acceptability of financial statements by global investors.

Why Ind AS?

Ind AS have many benefits, some of which are discussed below:

1. Wider acceptability:

Since Ind AS are converged form of IFRS which are widely acceptable and will give confidence to the user of financial statements.

2. Comparability of Financials:

Financial statements prepared using Ind AS are easily comparable with the financial statements prepared by companies of other countries.

3. Changes in standards as per economic situations:

Principles of Ind AS are revised/modified in case there is any major change in economy. Ind AS 29 is ‘Financial Reporting in hyperinflationary Economies’ which deals with situations related to inflation.

4. Attracts Foreign Investment:

Adopting Ind AS may attract foreign investors to invest in Indian Companies as that will ensure better comparability with similar companies across the globe.

5. Saves financial statement preparation cost:

For multinational companies, it will be beneficial as it will be able to use the same accounting standards in all the markets in which they operate. This will save preparation costs of aligning financial statements of Indian company with other operations.

Indian Accounting Standards Applicability:

Ind AS are applicable to specified category of companies as discussed below:

1. Mandatory requirement: Companies are required to follow Ind AS from Financial year 2015-2016. For Financial year 2018-19, following is the limit for companies required to follow Ind AS:

1. Companies whose equity or debt securities are listed or are in the process of being listed on any stock exchange in India or outside India;

2. Unlisted companies having net worth of Rs. 250 crore or more; and

3. Holding, subsidiary, joint venture or associate companies of companies covered in point (1) and (2) above.

In case of Non-Banking Financial Companies (NBFCs)

In 2018-19

1. NBFCs having net worth of rupees five hundred crore or more;

2. Holding, subsidiary, joint venture or associate companies of companies covered under point (1) above.

In 2019-20

1. NBFCs whose equity or debt securities are listed or in the process of listing on any stock exchange in India or outside India and having net worth less than Rs. 500 crore; 2. NBFCs, that are unlisted companies, having net worth of Rs. 250 crore or more but less than Rs. 500 crore; and

3. Holding, subsidiary, joint venture or associate companies of companies covered under point (1) and (2) above.

Voluntary applicability:

Company may voluntarily apply Indian accounting standards (Ind AS).

Requirement to follow AS:

Corporate entities are required to follow standard of accounting (Ind AS where applicable) while preparing its financial statements as per Section 129 of the Companies Act, 2013.

In case of conflict between Act and Indian Accounting standards:

In case there is any conflict between provisions of any applicable Act and Indian Accounting Standard (Ind AS), the provisions of the Act shall prevail to that extent.

International Financial Reporting Standards (IFRS)

International Financial Reporting Standards (IFRS) set common rules so that financial statements can be consistent, transparent, and comparable around the world. IFRS are issued by the International Accounting Standards Board (IASB). They specify how companies must maintain and report their accounts, defining types of transactions, and other events with financial impact. IFRS were established to create a common accounting language so that businesses and their financial statements can be consistent and reliable from company to company and country to country. IFRS are designed to bring consistency to accounting language, practices and statements, and to help businesses and investors make educated financial analyses and decisions. The IFRS Foundation sets the standards to “bring transparency, accountability and efficiency to financial markets around the world… fostering trust, growth and long-term financial stability in the global economy.” Companies benefit from the IFRS because investors are more likely to put money into a company if the company's business practices are transparent. IFRS are sometimes confused with International Accounting Standards (IAS), which are the older standards that IFRS replaced. IAS was issued from 1973 to 2000, and the International Accounting Standards Board (IASB) replaced the International Accounting Standards Committee (IASC) in 2001.

Standard IFRS Requirements

Comments